Is this Visa service provider poised for high growth

Is this Visa service provider poised for high growth

( An analysis on BLS international )

(This is not a stock recommendation please consult your financial advisor before investing)

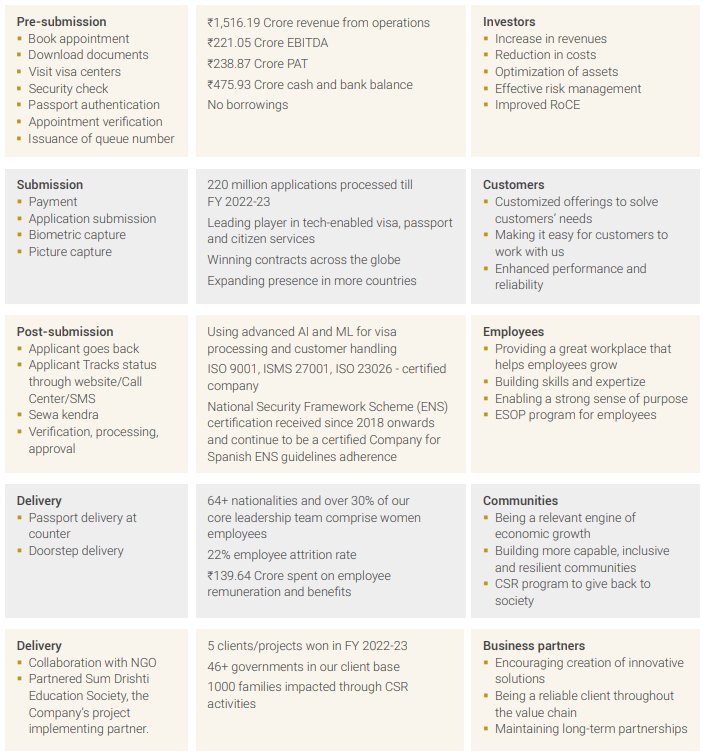

Part of the BLS group with four decades of experience BLS international is working in diversified sectors with its main business being in visa processing.

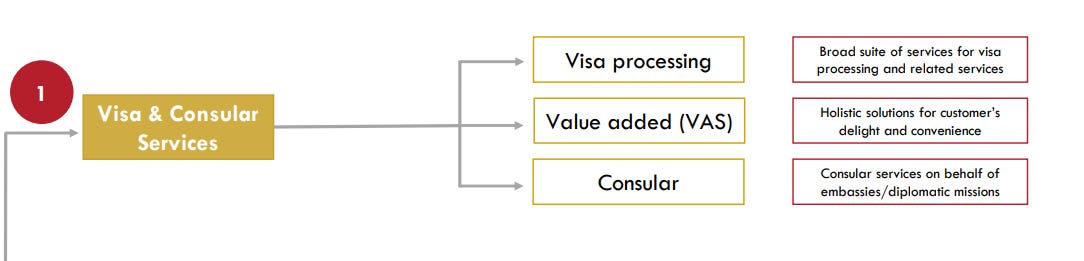

The company operates in two segments which are classified as follows

1 Visa & Consular Services which includes Visa, consular and VAS services

2 Digital Services which includes E-Gov Services, Banking correspondent and Assisted E-commerce.

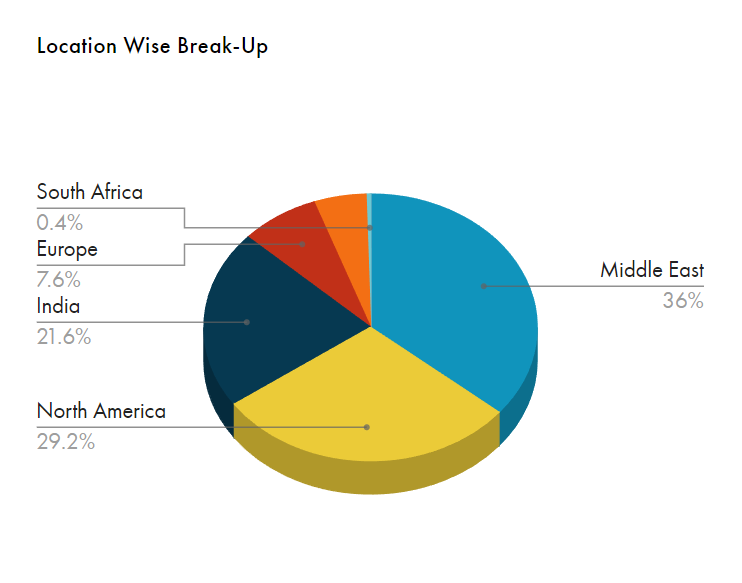

Company’s location wise break up

From the above chart we can conclude that middle east and north America constitute the larger chunk of its revenue.

We will be looking at each business segments in detail and why there lies an opportunity in the growing visa space.

The business model includes

Growth Triggers and Opportunities

A niche player in a highly oligopolistic market with a global market share of 15%. The market leader VFS global currently owns about 55-60% of the market share. Right now embassies in 2021 source 65% visa contracts in house and the rest are outsourced. With more outsourcing the number is expected to be 50-50 by 2025. BLS in its recent conference call said that there is a market opportunity of $1.5 billion in the coming two years.

High entry barriers

Very important to figure how the company or in general any company wins a contract. This process requires 70% technical knowledge and the rest 30% is determined by pricing power. With VFS Global which is the market leader in this segment embassies usually look for companies with some sort of experience which makes it a high entry barrier business. Company recently announced contracts with the Italian, Slovakian and the Thai government securing much higher rates.

High cash generating business

The company currently holds about 642 crores in cash which it requires for winning further contracts and partially to also look for M&A opportunities to grow its existing market share. With a positive CFO the company is also scouting for businesses which are in IT field and serving government organizations.

Growing digital services business

BLS plans to expand its digital business which is growing at about 140% YOY.

With acquisition of Zero mass private limited the company is now the largest partner to SBI with more than 12000+ Business correspondents to provide last mile banking solutions to rural India.

Focusing on the G2C business

The company is focusing on the G2C (Government to Consumer) business and aims to bring more state governments to provide services to the government by providing them with automation through cutting edge technology. Currently have contracts with Punjab, Rajasthan, Uttar Pradesh, Karnataka and West Bengal.

Zero debt and an Asset Light Model

The company currently has zero debt and operates on an Asset Light Model . Net debt free allows the company to take on cheaper debt if required to expand since it has a strong credit rating along with a high free cash flow business.

Potential Risks and threats

A highly regulated business that is susceptible to change with changes in government policies. The contracts with embassies are generally tender based and have certain conditions required such as experience in visa outsourcing, robust credit history, adequate information technology, operational expertise, and strong background check function.

This makes revenue susceptible to change and with unfavorable business acquisitions there could be an issue with the overall revenue risk profile of the group. Eg -Indian government had recently suspended travel to Canada

Consumer reviews and personal bias A simple Google search on the workings of BLS group will tell you how they usually overcharge customers and their customer service is not upto the mark. A customer oriented business will always succeed, however since the market is oligopolistic in nature and consumers have no where to go such slackness is usually found in companies especially those which are family owned and not run by professional management.

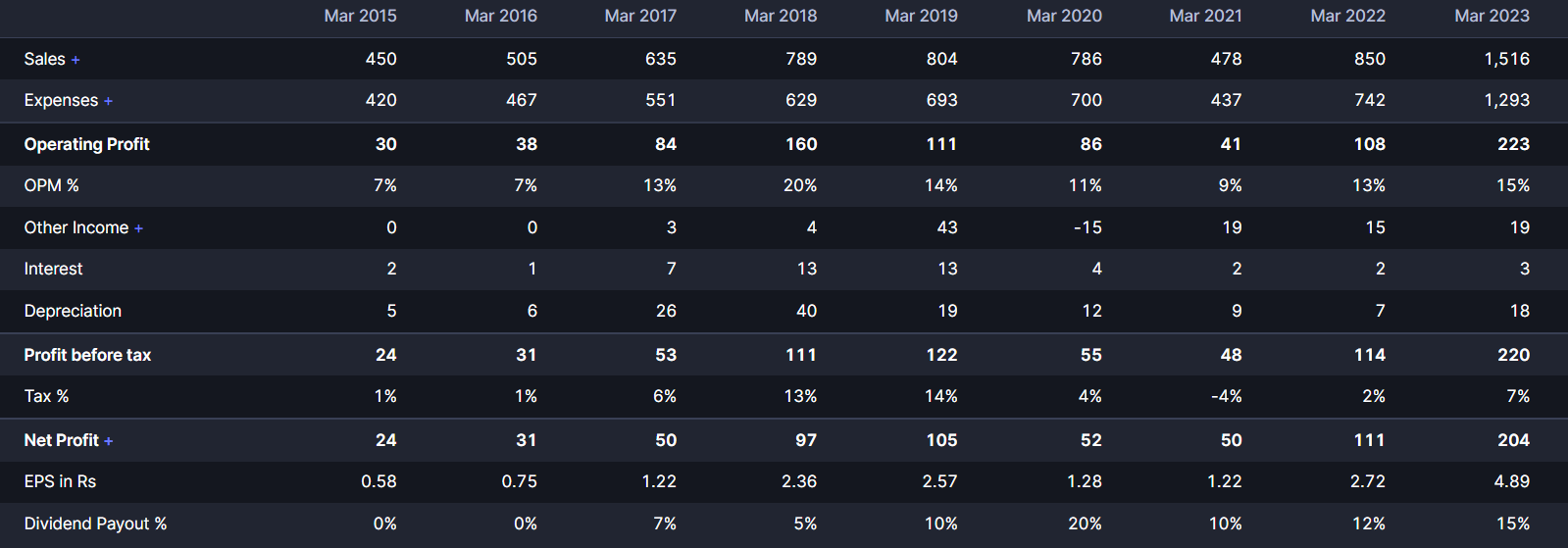

Analyzing the Financials

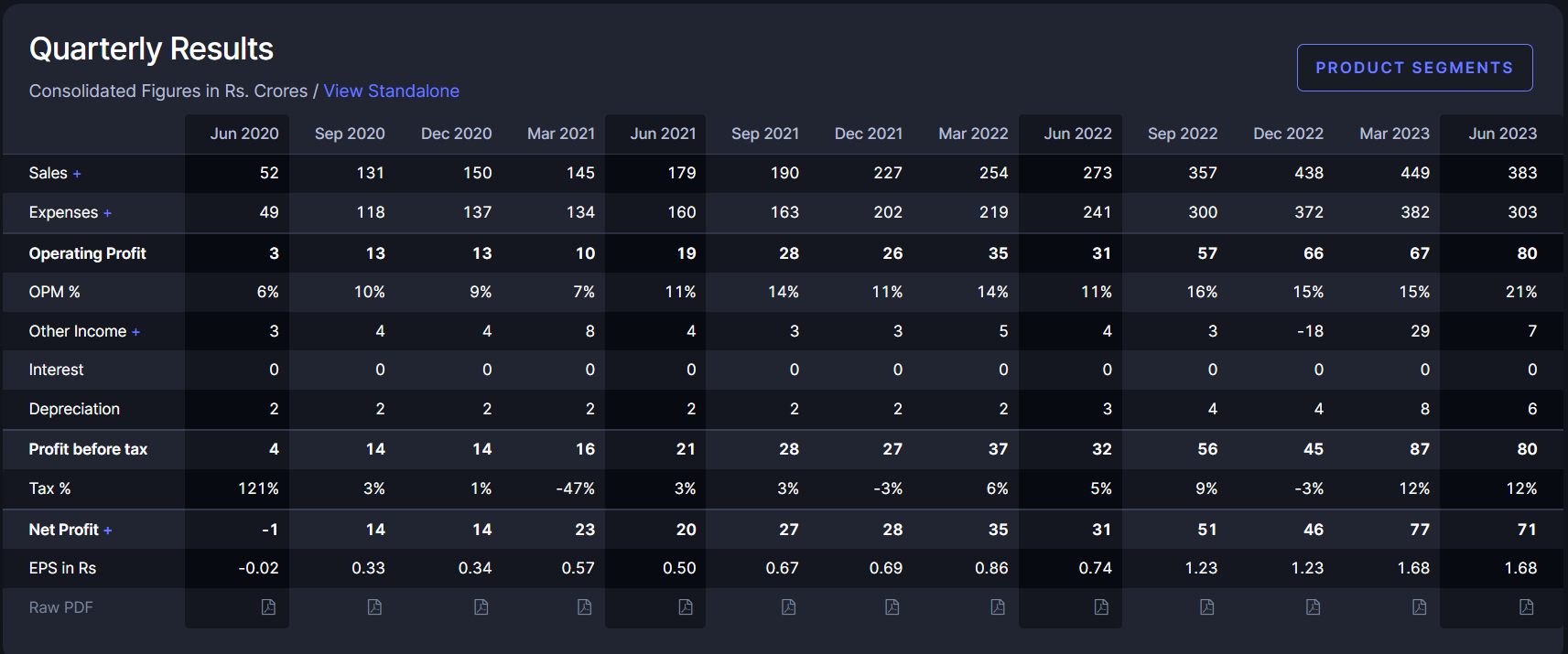

Quarterly PNL

Quarterly sales have been growing and YOY there has been a 40% increase in revenue with improved margins due to value added services being implemented like SMS services, insurance, premium lounges etc. Acquisition of Zero mass Pvt Ltd which is the largest business correspondent of SBI has also helped to increase margins. Travel levels have reached pre-covid and the company expects it to increase further with more demand for foreign travel along with a rising demand for international education among students. The opening of travel to China and Russia will increase revenue in the coming quarters as projected by the management.

YEARLY PNL

Sales are growing at an excellent rate exception of Covid year. Revenue is at an all time high with the company expecting a 20-25% growth in revenue this year. Margins have increased and expect them to increase further with the company growing its services by venturing into financial inclusion as well. Company has been following all required compliances which is necessary for the nature of the business.

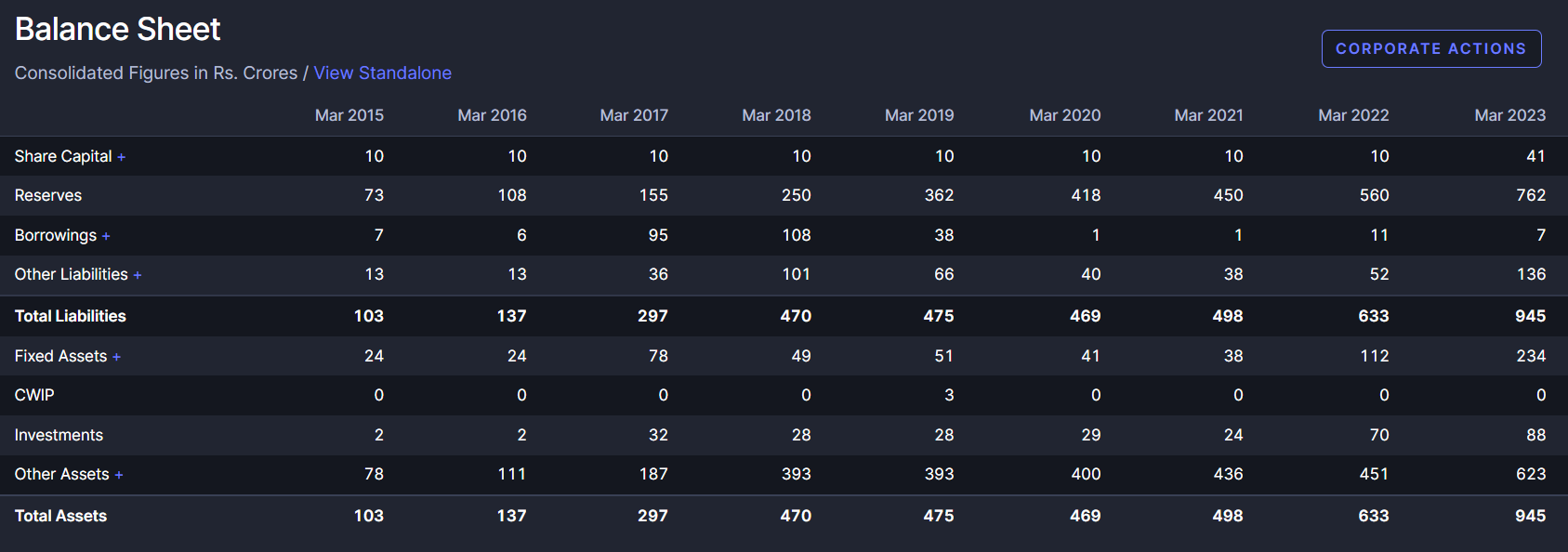

Balance Sheet

Increase in the balance sheet size proves the way the company is growing.

Borrowings have reduced with an increase in cash equivalents that will be used for further acquisitions. Company has a RoCe of 32% which signifies that the company is effectively managing its capital.

Other things to note

Company’s subsidiary BLS-E Services has filed for an ipo with SEBI. Valuation is still to be determined as the company is closely working with investment banks. Aims to raise about 290 to 320 odd crores through ipo which will be used for the E-services business only since the company does not want to use profits earned from the visa business to support growth of the e-services business. BLS will still hold more than 50% of the company and the money raised will be used to support the growth of the e services business through organic and inorganic acquisitions.

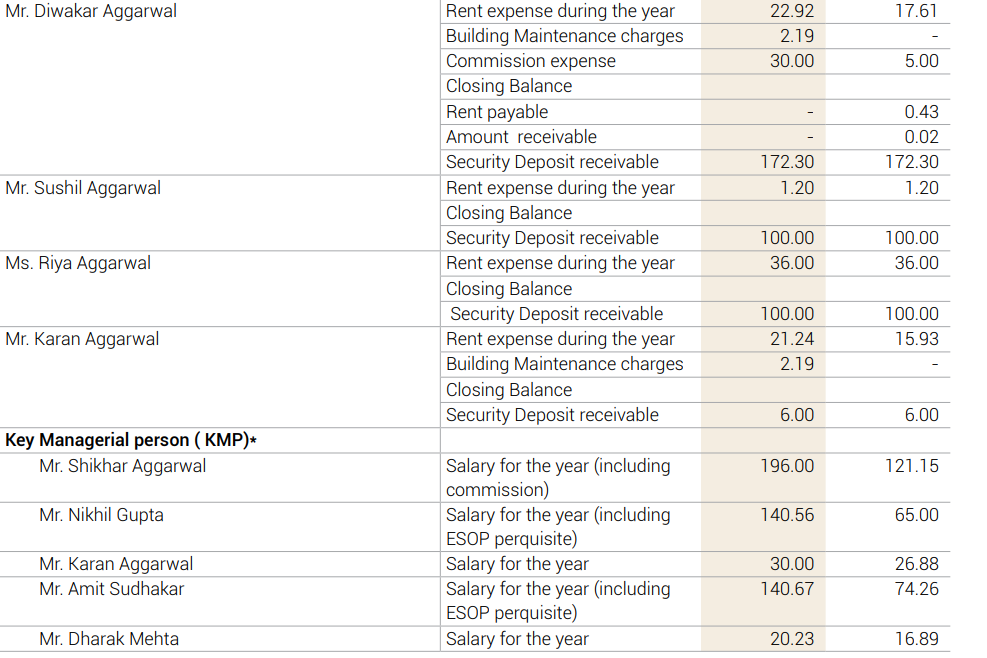

Related Party Transactions and Promoter background check

Considering the size of the business and the growth it achieved the related party transactions look fair and not over exaggerated with most of them comprising of rental allowance. Key management salaries total about 5 to 7 crores which isn’t too high for a business as this big but also not too low.

Mr Diwakar Aggarwal the chairman is the founder of BLS and is responsible for the growth of BLS through his visionary leadership.

Mr Nikhil Gupta a Chartered Accountant and the managing director of the company is responsible for the global visa business and its growth.

Mr Shikhar Aggarwal Joint MD joined the business in 2014. A bachelors degree from DU. No available information on what role does he actually play for the growth of the business.

Mr Karan Aggarwal executive director and a graduate in finance and management from the University of Bradford. Oversees the textile business of the group and has expanded it pretty well . Was also responsible for bagging the Punjab contract.

Stock Technicals

Past one year trend is positive with about 85% returns YTD. The stock is currently in an uptrend and the technicals suggest the stock to reach about 300 level which acts as a resistance. It will be interesting to watch if the stock breaks the 300 level with the company publishing its results for the September quarter on 6th Nov,2023. (Please note this is not a buy/sell recommendation, please consult your advisor before investing)

Overall the company seems to grow at a healthy rate with growing demand for travel services along with outsourcing of E-govt services. With little to no risks the company should grow in the near term.

If you liked this article please consider subscribing and sharing it with your friends and family.

If you seem to have any complaints or doubts please email me on cashflowing@substack.com and I would respond at the earliest.

Until then happy investing!

Disc : Invested ( Holding size 5.7%)